法的实施的直接目的是( )。

【不定项选择题】

背景资料

某综合楼工程,地下三层,地上二十层。总建筑面积约68000㎡。

施工单位进场后,项目技术负责人主持,项目部主要技术人员参加,编制了单位工程施工组织设计,内容包括编制依据、工程概况等。经施工单位技术负责人审批后,由项目生产经理组织,对相关人员就施工组织设计进行交底并作书面记录。项目部在施工过程中分阶段对施工组织设计的实施情况进行检查和验收。

该工程为泥浆护壁成孔灌注桩筏板基础,地基基础设计等级为甲级,灌注桩混凝土强度等级为C30,总计760根。根据合同约定,工程桩应进行承载力和桩身完整性检测,检测数量不得少于相应的规范要求。

手机使用

微信扫一扫

分享

参考答案

参考解析

【不定项选择题】

根据资料 (1),下列各项中,关于甲公司研发支出会计处理正确的是 ( )。

发生研发支出时,借记 “研发支出 —— 费用化支出” 科目 80000 元

发生研发支出时,借记 “研发支出 —— 资本化支出” 科目 80000 元

发生研发支出时,借记 “无形资产” 科目 80000 元

发生研发支出时,借记 “管理费用” 科目 80000 元

【不定项选择题】

【背景资料】

某河道治理工程施工1标建设内容为新建一座涵洞,指标文件依据《水利水电工程标准施工招标文件》(2009年版)编制,工程量清单采用清单计价格式。招标文件规定:

1.除措施项目外,其他工程项目采用单价承包方式。

2.投标最高限价490万元,超过限价的投标报价为无效报价。

3.发包人不提供材料和施工设备,也不设定暂估价项目。

投标截止时间为10天前,招标人未接到招标文件异议。在招标和合同管理发生如下事件:

事件1:投标人A提交的投标报价修改函及附件正本1份,副本4份,函明投标优惠5%,随同投标文件递交了投标保证金,投标保证金来源于工程所在省分公司资产,评标公示期结束后第二天,未中标的投标人A向该项目招标投标行政监督机构投诉,以投标最高限价违反法律法规为由,要求重新招标。

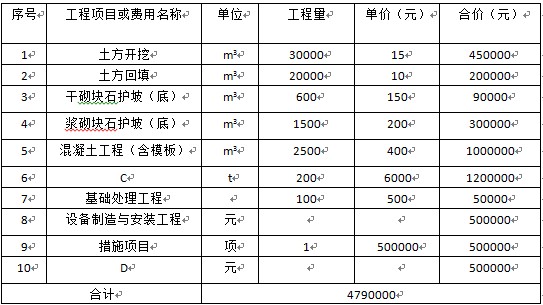

事件2:投标人B提交了已标价工程量清单(含已标价工程量清单计算附件)投标报价汇总如表3所示。

事件3:合同中关于砌体工程的计量和支付有如下约定:

1)砌体工程按招标图纸所示尺寸计算的有效砌筑体以m3为单位计量;

2)浆砌块石砂浆按有效砌筑体以m3为单位计量;

3)砌体工程中的止水设施排水管、垫层及预埋件等费用,包含在砌体项目有效工程量单价中,不另行支付;

4)承包人按合同要求完成砌体建筑物的基础清理和施工排水等工作所需费用包含在措施项目费用中,不另行支付。

【不定项选择题】

[A] Give compliments, just not too many.

[B]Put on a good face, always.

[C] Tailor your interactions.

[D] Spend time with everyone.

[E] Reveal, don’t hide, information.

[F] Slow down and listen.

[G] Put yourselves in others’ shoes.

Five Ways to Win Over Everyone in the Office

Is it possible to like everyone in your office? Think about how tough it is to get together 15 people, much less 50, who all get along perfectly. But unlike in friendships, you need coworkers. You work with them every day, and whether they’re your boss, direct report or equal, you depend on them just as they depend on you. Here are some ways that you can get the whole office on your side.

41. _______

If you have a bone to pick with someone in your workplace, you may try to stay tight-lipped around them. But you won’t be helping either one of you. A Harvard Business School study found that observers consistently rated those who were upfront about themselves more highly, while those who hid lost trustworthiness. The lesson is not that you should make your personal life an open book, but rather, when given the option to offer up details about yourself or studiously stash them away, you should just be honest.

42. _______

Just as important as being honest about yourself is being receptive to others. We often feel the need to tell others how we feel, whether it’s a concern about a project, a stray thought, or a compliment. Those are all valid, but you need to take time to hear out your coworkers, too. In fact, rushing to get your own ideas out there can cause colleagues to feel you don’t value their opinions. Do your best to engage coworkers in a genuine, back-and-forth conversation, rather than prioritizing your own thoughts.

43. _______

It’s common to have a “cubicle mate” or special confidant in a work setting. But in addition to those trusted coworkers, you should expand your horizons and find out about all the people around you. Use your lunch and coffee breaks to meet up with colleagues you don’t always see. Find out about their lives and interests beyond the job. It requires minimal effort and goes a long way. This will help to grow your internal network, in addition to being a nice break in the work day.

44. _______

Positive feedback is important for anyone to hear. And you don’t have to be someone’s boss to tell them they did an exceptional job on a particular project. This will help engender good will in others. But don’t overdo it or be fake about it. One study found that people responded best to comments that shifted from negative to positive, possibly because it suggested they had won somebody over.

45. _______

This one may be a bit more difficult to pull off, but it can go a long way to achieving results. Remember in dealing with any coworker what they appreciate from an interaction. Watch out for how they verbalize with others. Some people like small talk in a meeting before digging into important matters, while others are more straightforward. Jokes that work on one person won’t necessarily land with another. So, adapt your style accordingly to type. Consider the person that you’re dealing with before each interaction and what will get you to your desired outcome.

【不定项选择题】

【背景资料】

某小型水库除险加固工程的主要建设内容包括:土坝坝体加高培厚、新建坝体防渗系统、左岸和右岸输水涵进口拆除重建。依据《水利水电工程标准施工招标文件》编制招标文件。发包人与承包人签订的施工合同约定:(1)合同工期为210天,在一个非汛期完成;(2)签约合同价为680万元;(3)工程预付款为签约合同价的10%,开工前一次性支付,按 (其中F2=80%,F1=20%)扣回;(4)提交履约保证金,不扣留质量保证金。

(其中F2=80%,F1=20%)扣回;(4)提交履约保证金,不扣留质量保证金。

当地汛期为6~9月份,左岸和右岸输水涵在非汛期互为导流;土坝土方填筑按均衡施工安排,当其完成工程量达70%时开始实施土坝护坡;防渗系统应在2021年4月10日(含)前完成,混凝土防渗墙和坝基帷幕灌浆可搭接施工。承包人编制的施工进度计划如表3所示(每月按30天计)。

表3 水库除险加固工程施工进度计划

工程施工过程中发生如下事件:

事件1:工程实施到第3个月时,本工程的项目经理调动到企业任另职,此时承包人向监理人提交了更换项目经理的申请。拟新任本工程项目经理人选当时正在某河道整治工程任项目经理,因建设资金未落实导致该河道整治工程施工暂停已有135天,河道整治工程的建设单位同意项目经理调走。

事件2:由于发包人未按期提供施工图纸,导致混凝土防渗墙推迟10天开始,承包人按监理人的指示采取赶工措施保证按期完成。截至2021年2月份,累计已完成合同额442万元;3月份完成合同额87万元,混凝土防渗墙的赶工费用为5万元,且无工程变更及根据合同应增加或减少金额。承包人按合同约定向监理人提交了2021年3月份的进度付款申请单及相应的支持性证明。

【不定项选择题】

2017年1月,甲公司一批会计档案保管期满,其中有尚未结清的债权债务原始凭证。甲公司档案管理机构请会计机构负责人张某及相关人员在会计档案销毁清册上签署意见,将该批会计档案全部销毁。2017年9月,出纳郑某调离,与接替其工作的王某办理了会计工作交接。2017年12月,为完成利润指标,会计机构负责人张某采取虚增营业收入等方法,调整了财务会计报告,并经法定代表人周某同意,向乙公司提供了未经审计的财务会计报告。

要求:

根据上述资料,不考虑其他因素,分析回答下列小题。

【不定项选择题】

【背景资料】 甲、乙两家施工企业均具有施工总承包资质。两家企业组成联合体参加一铁路工程的投标,并签订了联合体协议。甲企业为联合体牵头单位。中标后,甲、乙两家企业分别与发包方签订了施工承包合同,并在承包合同中约定甲、乙两家企业分别就中标工程质量向发包方承担责任。

工程开工后,由于工期紧张,甲企业将部分工程(含主体工程)交给仅具有劳务承包资质的丙企业组织施工。乙企业将全部工程交给具有施工承包资质的丁企业组织施工。乙企业只收取管理费。

【不定项选择题】

根据资料 (1),下列各项中,关于甲公司短期借款相关会计处理正确的是 ( )。

按季支付利息时:借:财务费用 应付利息 贷:银行存款

取得借款时:借:银行存款 贷:短期借款

到期偿还短期借款时:借:短期借款 财务费用 贷:银行存款

计提 1 月、2 月的借款利息时:借:财务费用 贷:应付利息 0.06

【不定项选择题】

根据资料 (1), 下列各项中,关于甲公司 6 月 5 日的会计处理正确的是 ( )。

借 :在途物资 60 应交税费 —— 应交增值税 (进项税额) 7.8 贷:应付账款 67.8

借:材料采购 60 应交税费 —— 应交增值税 (进项税额) 7.8 贷:银行存款 67.8

借:在途物资 60 应交税费 —— 应交增值税 (进项税额) 7.8 贷:银行存款 67.8

借:原材料 60 应交税费 —— 应交增值税 (进项税额) 7.8 贷:银行存款 67.8

【不定项选择题】

甲因其丈夫在公安局看守所工作,所以与看守所的监管人员都很熟悉。一天,甲收受在押重刑犯乙的亲戚3万元钱,在没有和丈夫商量的情况下,利用自己出入看守所的方便,帮助乙从看守所逃走。甲的行为构成( )。

受贿罪。

私放在押人员罪。

脱逃罪。

私放在押人员罪和受贿罪。